Federal Budget: 2021

On April 19, 2021 (Budget Day) Finance Minister Chrystia Freeland announced the first budget presented by the government in two years, “A Recovery Plan for Jobs, Growth, and Resilience”. The Budget indicates that the deficit for the 2020-2021 year was $354 billion, anticipates a deficit of $154 billion for 2021-2022 fiscal year and projects that the deficits will drop to $25 billion by 2025. The federal debt is forecast to double to $1.441 trillion by 2025.

The major spending announcements in the budget include a $30 billion childcare plan with the aim of reaching an average cost of $10 per day, $18 billion to support Indigenous people, $17.6 billion invested in the green economy and $3.9 billion towards reforming Employment Insurance. Also included is an increase to Old Age Security for those 75 or over.

Other measures include establishing a $15 per hour federal minimum wage, extending the waiver on student debt until 2023 and extending COVID-19 business support through existing and new programs.

The tax changes announced in Budget 2021 do not include any major tax increases but do have several targeted new taxes including taxes on digital sales and luxury goods. A welcome surprise is a complete write-off of most purchases of capital assets other than buildings and intangibles.

See all details of the key tax highlights of the budget in the document below.

PERSONAL INCOME TAX MEASURES

Disability Tax Credit

Budget 2021 proposes to make it easier to claim the Disability Tax Credit (DTC) by relaxing some of the conditions currently required to claim it. In order to claim the DTC a person has to have a marked restriction in an aspect of everyday life. Two categories that are relatively difficult to qualify for under the current rules are mental functions and a requirement for time consuming, life-sustaining therapy (i.e., dialysis).

Under the current rules, mental functions necessary for everyday life include memory, problem-solving, goal-setting and judgement (taken together), and adaptive functioning.

Under the current rules, time spent on receiving life-sustaining therapy includes activities that require the individual to take time away from everyday activities to receive the therapy, activities directly involved in determining the appropriate dosage for medicine, and the time spent by a child’s primary caregivers to perform and supervise these activities for the child.

Budget 2021 proposes to expand on these requirements as follows:

- Mental functions necessary for everyday life now include several other factors including attention, perception of reality, problem-solving and regulation of behaviour and emotions.

- Time spent on therapy will include time spent by an assistant, time spent determining dietary intake, medicines and/or physical exertion to be considered part of the therapy. The requirement for therapy to be administered three times each week will be reduced to two times each week provided the 14 hour per week requirement is met.

These changes as proposed would apply to 2021 and subsequent taxation years, in respect of DTC certificates filed with the Minister of National Revenue on or after Royal Assent.

Tax Treatments of COVID-19 Benefit Amounts

Currently, where a benefit amount such as CERB is repaid, the repayment can only be deducted for income tax purposes in the year the repayment takes place. Therefore, if the repayment does not occur in the same year as the year of receipt of the benefit, an individual may owe tax in respect of the benefit for the year of receipt, while obtaining a deduction for the repayment amount in a future tax year.

Budget 2021 proposes to amend the Income Tax Act to ensure COVID-19 benefit amounts that were repaid in a subsequent year may instead be deducted in the year the benefit was received. In addition, Budget 2021 proposes to amend the Income Tax Act to ensure that COVID-19 benefits received are included in taxable income of those individuals who reside in Canada but are considered non-resident persons for income tax purposes.

These changes as proposed would apply to amounts repaid anytime prior to 2023.

Electronic Filing and Certification of Tax and Information Returns

Budget 2021 proposes several amendments to the various acts to improve Canada Revenue Agency’s (CRA) ability to operate digitally to provide faster and secure service.

Budget 2021 proposes to make the following changes:

- To allow CRA to send notices of assessment electronically without taxpayer consent;

- Change the default correspondence for businesses that use the CRA’s My Business Account portal to electronic with the option to change to paper;

- Issuers of T4A and T5 slips may provide them electronically;

- Mandatory electronic filing of income tax information returns reduced from 50 to 5 slips;

- To essentially require all corporations to electronically file income tax and GST/HST returns;

- Electronic payments for tax remittances over $10,000; and

- To eliminate the requirement that signatures be in writing for form T183 to authorize E-Filing of a return and T2200, Declaration of Conditions of employment

Most of these changes would come into force for periods after 2021. The waiving of the requirement for handwritten authorization will occur on Royal Assent of the enacting legislation.

Other Measures

Budget 2021 also proposes the following changes:

- Increase the availability of the Canada Workers’ Benefit;

- Enhance the travel deduction for the Northern Residents’ deduction;

- Retroactively include post-doctoral income in “earned income” when determining RRSP room;

- Allow deductions for contributions to defined contribution pension plans for certain prior years;

- Improve CRA’s ability to revoke charitable status where

- the charity or an officer are linked to a terrorist organization, by expanding the definition of “ineligible individual”;

- a false statement amounting to culpable conduct was made for the purpose of maintaining registration.

BUSINESS INCOME TAX MEASURES

Emergency Business Support Programs

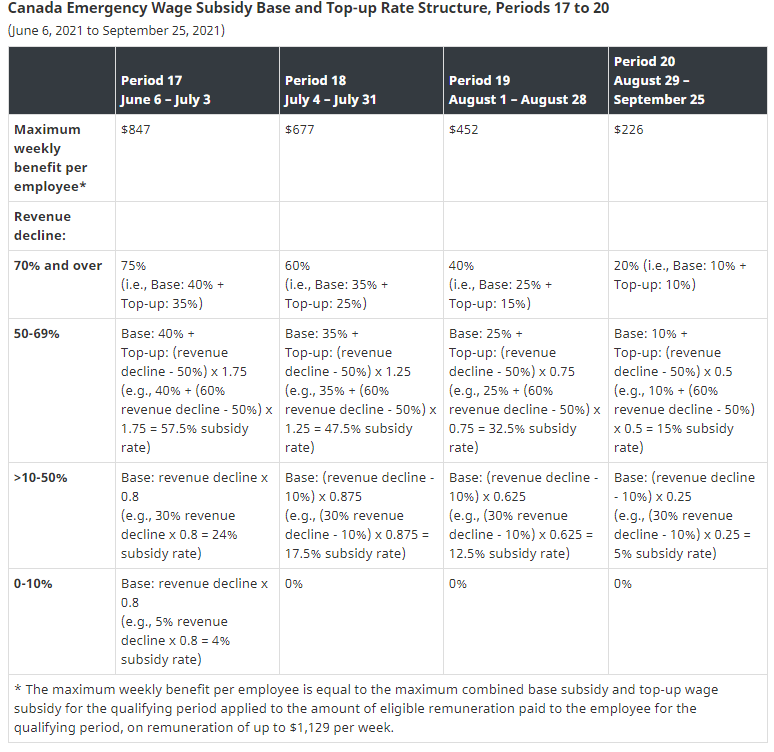

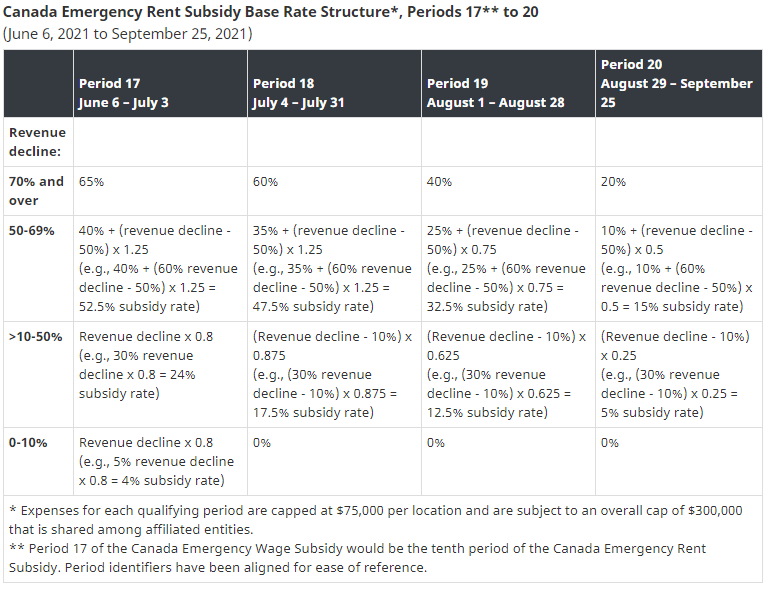

During the pandemic, the government has introduced a number of support programs for businesses in order to financially assist with certain expenses and outlays including the Canada Emergency Wage Subsidy (CEWS) and the Canada Emergency Rent Subsidy (CERS). Both of these programs are currently scheduled to cease on June 5, 2021.

Budget 2021 proposes to extend both the CEWS and CERS program durations. Both programs are proposed to be extended until September 25, 2021, with legislative authority to further extend the programs to November 20, 2021 if deemed necessary.

After June, subsidy rates will be reduced and phased out each period, and commencing July 4, 2021, only businesses experiencing a greater than 10% decline in revenue will be eligible. The proposed phase out rates are as shown in the following tables:

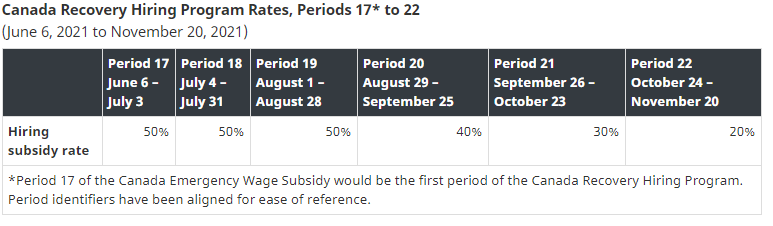

Canada Recovery Hiring Program (CRHP)

Budget 2021 introduces a new subsidy program for eligible employers. For a given period, employers may apply for either this new subsidy, or the Canada Emergency Wage Subsidy (CEWS), whichever is preferable. The program will be in effect for remuneration paid to eligible employees between June 6 and November 20, 2021.

Eligibility:

- Employers who are already eligible for CEWS would generally be eligible for this hiring subsidy.

- Employees must be employed primarily in Canada by an eligible employer throughout the qualifying period. The employee must not be a furloughed employee (that is, on leave with pay, except for paid absences such as vacation, sick leave or sabbatical).

- Eligible remuneration generally includes salary and wages, but does not include amounts such as severance pay, stock options, or personal use of a corporate vehicle. The remuneration must relate to the qualifying period.

How the hiring subsidy works:

- Similar to CEWS, for each period revenue is compared to a baseline period, which is either the same calendar month pre-pandemic, or the average of revenue in January 2020 and February 2020.

- If revenue has declined in excess of a revenue-decline threshold, then an eligible employer may apply. The thresholds are 0% (i.e., any revenue decline at all) for the period of June 6 to July 3, 2021, and 10% for periods between July 4 to November 20, 2021.

- The subsidy available is equal to the increase in remuneration paid compared to a baseline period, namely March 14 to April 10, 2021, times a subsidy rate. The subsidy is capped at $1,129 per week.

Proposed subsidy rates under this program are as follows:

Immediate Expensing of Certain Capital Property

Acquisitions of depreciable capital property are added to a “Capital Cost Allowance” (CCA) class, which is a pool that allows for the cost of the property to be claimed over time at a prescribed rate.

Budget 2021 proposes to allow immediate expensing of certain acquisitions of capital property acquired by Canadian-Controlled Private Corporations (CCPC) rather than claiming the cost over time, up to a maximum amount of $1.5 million per year. If in the year, there is more than $1.5 million worth of eligible property acquired, the excess amount over $1.5 million will be subject to normal CCA rules.

Eligible property would be most capital property except for most buildings, paving and intangible assets.

The eligible property must be acquired by the CCPC on or after Budget Day and become available for use before January 1, 2024

Rate Reduction for Zero-Emission Technology Manufacturers

Budget 2021 proposes a temporary measure to reduce corporate income tax rates for qualifying zero-emission technology manufacturers. Specifically, taxpayers would be able to apply reduced tax rates on eligible zero-emission technology manufacturing and processing income of:

• 7.5 per cent, where that income would otherwise be taxed at the 15 per cent general corporate tax rate; and

• 4.5 per cent, where that income would otherwise be taxed at the 9 per cent small business tax rate.

Budget 2021 proposes to introduce these rates for taxation years beginning on or after January 1, 2022. These rates would be phased out starting in 2029 through to 2031.

Capital Cost Allowance for Clean Energy Equipment

To support investment in clean technologies, Budget 2021 proposes to expand Classes 43.1 and 43.2 to include the following:

• hydroelectric storage and generation equipment;

• active solar and geothermal heating systems for a swimming pool;

• equipment used to produce solid and liquid fuels (e.g., wood pellets and renewable diesel) from specified waste material or carbon dioxide; and

• a broader range of equipment used for the production and dispensing of hydrogen.

INTERNATIONAL TAX MEASURES

Interest Deductibility Limits

The government is concerned that excessive debt or interest expense can be placed in Canadian businesses in a way that erodes the tax base, for example, through:

- interest payments to related non-residents in low-tax jurisdictions;

- the use of debt to finance investments that earn non-taxable income; or

- having Canadian businesses bear a disproportionate burden of a multinational group’s third-party borrowings.

Budget 2021 proposes to introduce an earnings-stripping rule that limits the amount of “net interest expense” that may be deducted to a fixed share of earnings. The new rule would limit the amount of net interest expense that a corporation may deduct in computing its taxable income to no more than a fixed ratio of “tax EBITDA”.

Exceptions include Canadian Controlled Private Corporations (CCPC) (or groups of associated CCPCs) with taxable capital of less than $15 million, and groups of corporations with net interest expense of less than $250,000. Interest income and expenses between Canadian members of a related group would also be excluded.

Where interest is not deductible, the provisions include the ability to either transfer them to another member of the Canadian group, carry the expense back three years or carry them forward twenty years.

This provision will be phased in, with a fixed ratio of 40 per cent for taxation years beginning on or after January 1, 2023 but before January 1, 2024 (the transition year), and 30 per cent for taxation years beginning on or after January 1, 2024.

SALES AND EXCISE TAX MEASURES

Application of the GST/HST to E-commerce

The government previously proposed a number of changes to the Goods and Services Tax/Harmonized Sales Tax (GST/HST) with respect to the digital economy to ensure HST will be collected on sales by or through distributers such as Amazon, Netflix and AirBnB effective July 1, 2021. Budget 2021 included additional technical provisions with respect to those new taxes.

Tax on Select Luxury Goods

Budget 2021 proposes to introduce a 10 to 20 per cent tax on the retail sale of new luxury cars and personal aircraft priced over $100,000, and boats priced over $250,000, effective as of January 1, 2022.

Luxury Vehicles: Includes all new passenger vehicles typically suitable for personal use if they are equipped to accommodate less than 10 passengers. Excluded vehicles include certain motorcycles, off-road vehicles, motor homes, construction vehicles, farm vehicles and public sector vehicles (including hearses).

Aircraft: It is proposed that the tax apply to all new aircraft typically suitable for personal use, including aeroplanes, helicopters and gliders.

Boats: It is proposed that the tax apply to new boats such as yachts, recreational motorboats and sailboats, typically suitable for personal use.

Further details will be announced in the coming months.

Other Measures

Other measures include:

- Allowing the GST new housing rebate to be claimed when multiple unrelated owners acquire a property;

- Increase the thresholds for requiring information on receipts to claim a GST/HST Input Tax Credit to $100 (from $30) and $500 (from $150);

- Increase the Excise Duty on Tobacco;

- Implement a new tax on vaping products;

- Requiring goods to be valued using the last sale to Canada for the purpose of calculating tax and duties.

If you have any questions concerning the above, do not hesitate to contact your trusted advisor at Wilkinson & Company LLP.

This summary deals with proposed matters that are complex and may not apply to particular facts and circumstances. As well, the material and the references contained therein reflect laws and practices which are subject to change. For these reasons, this material should not be relied upon as a substitute for specialized professional advice in connection with any particular matter.

Although this communication has been carefully prepared, Wilkinson & Company LLP does not accept any legal responsibility for its contents or for any consequences arising from its use. No part of this document may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means (photocopying, electronic, mechanical, recording or otherwise).