Changes to T4/T4A Reporting

We are here to inform you of important new filing requirements that will affect all employers that prepare T4 or T4A slips.

Requirement to Report Dental Benefits

The Canadian Dental Care Plan (CDCP) was introduced in November 2022 and expanded in June 2023 to include more individuals. Currently only those aged 12 and under are eligible. Individuals over the age of 70 may apply beginning March 2024, those over 64 may apply as of May 2024, and children under 18 and adults with a valid Disability Tax Credit (DTC) certificate may apply in June 2024. More information on the CDCP may be found on the Canada Revenue Agency’s website.

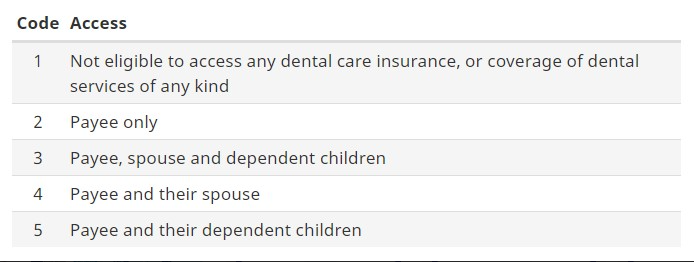

Given that the CDCP will generally only apply to those without existing dental insurance, the CRA requires details of who is, or could be, covered. As such, for 2023 T4 and/or T4A slips employers must report whether an active employee or any of their family members were eligible on December 31 to access any dental care insurance, or coverage of dental services of any kind offered by the employer.

This information is to be reported in Box 45 – Employer-offered Dental Benefits for T4 slips, or Box 015 – Payer-offered Dental Benefits on T4A slips. Completion of Box 015 is required if an amount is reported in Box 016, Pension or Superannuation. The following codes should be used:

It is important to be aware that Code 1 cannot be used if the employee or their family could take part in a dental plan. For instance, Code 1 cannot be used for an employee that opts out of, or chooses not to participate in, an available dental plan.

For 2023 slips only, T4 Box 45 and/or T4A Box 015 do not need to be completed if the applicable code is “1” and reasonable efforts are made to comply with the requirements. Slips filed prior to January 2024 do not need to be amended.

More information can be found on the CRA’s T4 guide in the instructions for Box 45.

If we will be preparing your T4 or T4A slips and returns please include the responses to these questions with your information.

Mandatory Electronic Filing

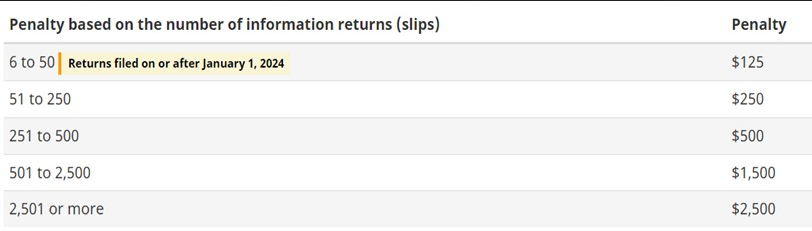

As we previously communicated, commencing January 1, 2024, the CRA will lower the threshold for electronic filing information slips such as T4s and T5s from fifty (50) to six (6). Any entity filing 6 or more information returns (slips and summaries) must file electronically rather than submitting paper copies by mail.

Examples of information returns include the T4 payroll return (renumeration paid), T5 (investment income), T3 (trust income) and T4A (pension and other income return).

If the slips or summaries are not filed electronically penalties will be applied depending on the number of slips submitted as follows:

The CRA’s news release on the subject contains instructions on several methods to electronically file the information returns. Alternatively, we can electronically file your returns on your behalf as your representative.

If you have any questions, please contact your advisor at Wilkinson & Company LLP