CLIENT UPDATE – Regional Opportunities Investment Tax Credit

The 2020 Ontario budget introduced a 10% tax credit for capital investments towards most buildings, made by a qualifying corporation on or after March 25, 2020. The 2021 Ontario Budget enhanced this credit to 20% for eligible expenditures after March 24, 2021 and before January 1, 2023. Most recently (September 8, 2022) the end date of the enhanced credit was extended to eligible expenditures available for use prior to January 1, 2024.

This tax credit would be available for eligible expenditures of a minimum $50,000 to a maximum of $500,000, allowing for a maximum tax credit of $90,000. A qualifying corporation may have more than one eligible expenditure in the year, however, overall the tax credit is capped at $90,000.

To be eligible for this tax credit you must have a qualifying corporation, have made an eligible expenditure and not meet one of the exceptions.

QUALIFYING CORPORATION

To be eligible for the tax credit the corporation must be:

- A Canadian Controlled Private Corporation (CCPC);

- Not be tax exempt; and

- Carry on business in Ontario through permanent establishment in Ontario

ELIGIBLE EXPENDITURE

An eligible expenditure is eligible property that became available for use on or after March 25, 2020, while the corporation was a qualifying corporation. For the enhanced credit, the eligible property must have become available for use after March 24, 2021 and before January 1, 2024.

ELIGIBLE PROPERTY

Eligible property is generally a commercial building or an addition or improvement to a commercial building, where at least 90 per cent of the floor space of the building is used at the end of the taxation year for non-residential purposes. More specifically, it is a depreciable property identified as either Class 1 or Class 6 of Schedule II in the Income Tax Regulations section of the Income Tax Act. Please note, upon applying for the tax credit, the Class 1 or Class 6 class is reduced by the amount of the tax credit received which reduces the future tax deduction for depreciation purposes.

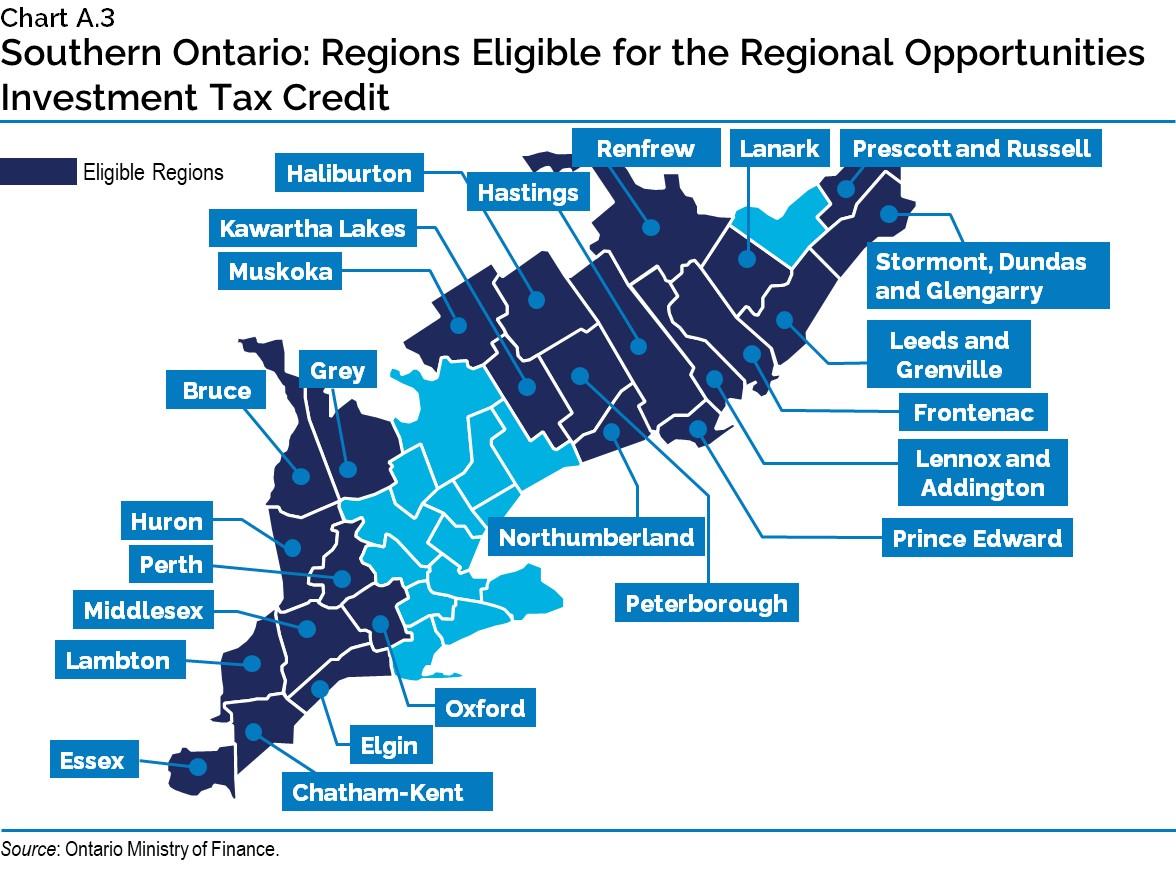

The eligible property must be located in a qualifying region, as shown in the map below.

EXCEPTIONS

However, no credit is allowed if the eligible property was acquired from non-arm’s length sellers or in circumstances where it was previously owned by non-arm’s length person. Generally, a non-arm’s length person is someone who is related to the purchaser, or a corporation controlled by someone related.

Further, no credit is allowed if the property was acquired from a person or partnership, who has a right or option to reacquire all or part of the property in the future or who has granted a right or option to any other person or partnership to reacquire the property in the future.

ASSOCIATED CORPORATIONS

Additional rules are applicable for those corporations which are associated. The tax credit will be nil for a qualifying corporation, UNLESS each of the other corporations in the associated group waive their tax credit entitlement for any taxation year that overlaps with the qualifying corporation’s taxation year. If you are unsure whether you have an associated corporation, please speak with your trusted advisor.

If you have any questions concerning the above, do not hesitate to contact your trusted advisor at Wilkinson & Company LLP.

This summary deals with proposed matters that are complex and may not apply to particular facts and circumstances. As well, the material and the references contained therein reflect laws and practices which are subject to change. For these reasons, this material should not be relied upon as a substitute for specialized professional advice in connection with any particular matter.

Although this communication has been carefully prepared, Wilkinson & Company LLP does not accept any legal responsibility for its contents or for any consequences arising from its use. No part of this document may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means (photocopying, electronic, mechanical, recording or otherwise).