CLIENT UPDATE – Canada Emergency Rent Subsidy (CERS) – Application

November 27, 2020

This communication is intended to provide you with a detailed update regarding the Canada Emergency Rent Subsidy (CERS), specifically the eligibility requirements and application process.

On November 23, 2020, the CRA application for the CERS came online. As noted in our previous communications, this program will be replacing the Canada Emergency Commercial Rent Assistance (CECRA) programs operating by the federal and provincial governments.

The main difference from the CECRA program is that tenants and property owners can apply for the subsidy, although each have a different calculation that is to be used. This resolves one of the major complaints about the previous program in that the landlord’s consent is no longer required. Property owners will generally only be eligible to claim the subsidy if they use a property in their business or lease it to a non-arm’s length party who uses it in their business.

The determination for eligibility and the calculation of the subsidy to be paid are very similar to the Canada Emergency Wage Subsidy (CEWS) in that eligibility is determined by comparing revenue against a prior period, and the subsidy rate is impacted by the extent of the revenue change.

The following discussion should help you determine if you are eligible, for how much, and how to apply.

Eligible Entities

Eligible entities include individuals, taxable corporations and trusts, non-profit organizations and registered charities. Public institutions are generally not eligible for the subsidy (such as municipalities, public universities, colleges and schools, crown corporations and hospitals).

Eligible entities also include the following groups:

- Partnerships that are up to 50 per cent owned by eligible members;

- Indigenous government-owned corporations that are carrying on a business, as well as partnerships where the partners are Indigenous governments and eligible entities;

- Registered Canadian Amateur Athletic Associations;

- Registered Journalism Organizations; and

- Non-public colleges and schools, including institutions that offer specialized services, such as arts schools, driving schools, language schools or flight schools.

In addition, an eligible entity must meet one of the following criteria:

- Have a payroll account as of March 15, 2020 or have been using a payroll service provider;

- Have a business number as of September 27, 2020 (and satisfy the Canada Revenue Agency that it is a bona fide rent subsidy claim);

- You purchased the business assets of another person or partnership who meets condition 2 above and have made an election under the special asset acquisition rules

- These special asset acquisition rules are the same for the Canada Emergency Wage Subsidy (CEWS); or

- You meet other conditions that may be prescribed in the future.

The Subsidy Rate

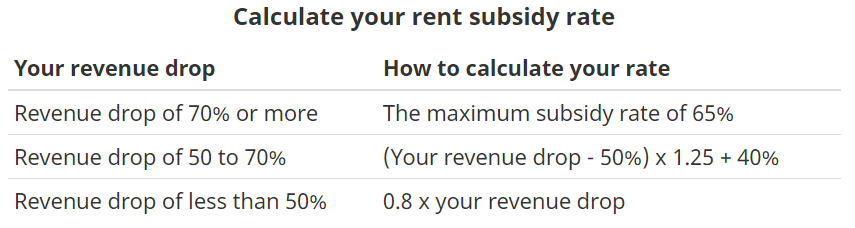

The Base Subsidy

This subsidy rate and claw-back mirrors that of the CEWS. The maximum base rate subsidy is 65% for organizations with a revenue decrease of 70% or more. The base rate would then decline to a rate of 40% for organizations with a revenue drop of 50%, and then would gradually reduce to zero for those not experiencing a decline in revenues.

Expenses for each qualifying period would be capped at $75,000 per location and be subject to an overall cap of $300,000 which would be shared among affiliated entities. There is no such limitation provided for the CEWS program. The use of “affiliated” rather than “associated” should be noted by those preparing these applications as the terms have different meanings under the Income Tax Act.

An agreement, in prescribed form, must be filed by affiliated parties to share the $300,000 expenditure limit. It appears this form is part of the application process discussed later in this document.

There are special rules for determining revenue similar to those available for CEWS. This is also discussed in more detail later in this document.

Lockdown Support Top-Up

An additional 25% top-up will provide additional support to entities temporarily forced to close or whose business activities are significantly restricted due to a mandatory public health order in effect for a period of at least a week, including a mandatory shutdown resulting from an outbreak of COVID-19. If the public health restriction is in effect for only part of a qualifying period, the lockdown support top-up will be pro-rated for the number of days that the business was affected.

In order to qualify for the additional 25% top-up, an entity must first qualify for the base CERS and then have had one or more locations temporarily closed, or have activities significantly restricted for a week or longer due to a COVID-19 related public health order. The impacted activities as a result of the public health order must account for at least 25% of total revenues at that location during the prior reference period. An order that restricts or reduces activities but does not require you to close or stop the activities does not qualify for the enhanced lockdown support. The 25% top-up is limited to $75,000 per qualifying property, however, unlike the base rate subsidy, is not subject to the overall cap.

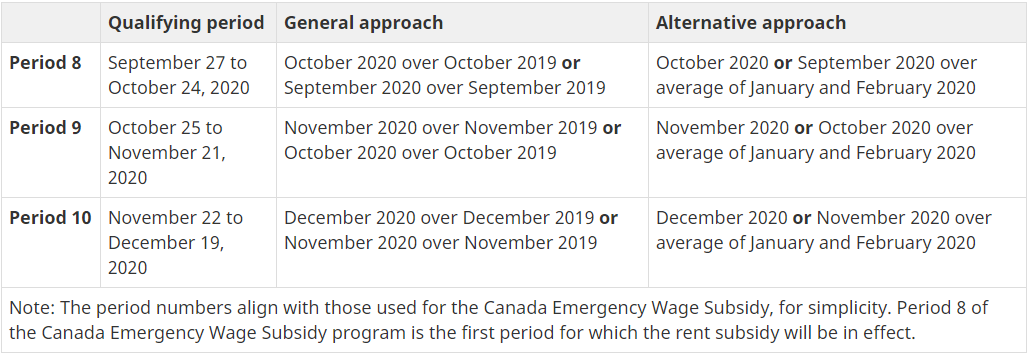

Eligible Periods

The CERS will be available for periods from September 27, 2020 through to June 2021. The CERS “qualifying periods” are the same as those used for CEWS (starting at Period 8 of the CEWS program).

To determine if an entity is eligible for a period, they must compare their revenue for a month to either a comparable period in 2019, or the average of January and February 2020. The following chart summarizes the current eligible periods and the revenue comparison to be used for each:

All applications must be made on or before 180 days after the end of the qualifying period.

The current legislation only provides for eligibility criteria and subsidy rates from periods through to December 19, 2020. It seems reasonable to assume that the 2021 rules for both CERS and CEWS will be similar and are likely to be announced at the same time.

Eligible Expenses

A tenant’s expenses eligible for the subsidy include:

- Commercial rent and most related payments, paid to arm’s-length parties,

- Operating expenses, such as insurance, utilities and common area maintenance expenses, customarily charged to the lessee under a net lease, and

- Property taxes (including school taxes and municipal taxes).

Any sales tax (e.g., GST/HST) component of these costs would not be an eligible expense. Also excluded are most payments for damages, guarantees, interest and penalties.

A property owner may only claim the subsidy where the property is not primarily used to earn rental income from arm’s length parties. As such, a property owner that uses the property in their own active business will qualify, as will a property owner that leases the property to a non-arm’s length commercial business. Residential rent received from non-arm’s length parties does not qualify.

A tenant renting from a non-arm’s length party will not be able to claim the subsidy for the rent payments as payments between non-arm’s length parties are not eligible expenses.

A property owner’s expenses eligible for the subsidy include:

- Mortgage interest,

- Limited to the extent of the lesser of the cost amount of the property and the lowest principal amount at any time since the property was acquired

- Insurance, and

- Property taxes (including school taxes and municipal taxes).

Eligible expenses would be limited to those paid under agreements in writing entered into before October 9, 2020 (and continuations of those agreements) and would be limited to expenses related to real property located in Canada. Expenses that relate to residential property used by the taxpayer (e.g., their house or cottage) would not be eligible. Payments made between non-arm’s length entities would not be eligible expenses. As such, rent paid to a non-arm’s length party cannot be claimed, the landlord would need to claim the appropriate amount for their eligible costs instead.

Expenses must have been paid or will be paid within 60 days after the payment of the first subsidy amount to which those expenses relate.

Determining Revenue

The method of determining the revenue reduction for CERS is fortunately the same as it is for CEWS. It also appears that an election to use one of the alternate methods of determining revenue must be consistent between the two programs.

An entity must follow its normal accounting policy for determining revenue, except that revenue from non-arm’s length parties are excluded.

The following is a summary of the available elections relevant to the CERS program:

- To use the cash method instead of the accrual method or the accrual method instead of the cash method;

- To determine revenues on a consolidated basis, for those that normally do not consolidate;

- To determine revenues on a non-consolidated basis, for those that normally consolidate;

- For entities that earn all or substantially all of their revenue from non-arm’s length parties, an election to use the revenues of those parties instead of their own;

- To use the revenue of an eligible joint venture;

- Entities that have acquired at least 90% of the assets of another business may file a joint election to include the acquired business’s prior revenues in their calculations; and

- A charity or not-for-profit can elect to exclude government funding.

How to Apply

Applications may be made online by the eligible applicant through “My Business Account” or by their authorized representatives at this website.

You will need to provide:

- The revenue reduction percentage;

- The total amount of eligible expenses;

- Name and contact info of:

- Mortgage holder if you have a mortgage on the property; or

- Landlord if you rent the property

- If there are affiliated entities:

- The percentage of the $300,000 limit assigned to each entity; and

- The CRA business number (BN) of each affiliated entity

- If a representative is making the claim for you, a signed attestation confirming the details of the application and the related elections.

The subsidy is expected to be paid within 4-8 business days of the application.

If you have any questions concerning the above, do not hesitate to contact your trusted advisor at Wilkinson & Company LLP.

To review any of our previous updates on COVID-19 please see our website.

This summary deals with proposed matters that are complex and may not apply to particular facts and circumstances. As well, the material and the references contained therein reflect laws and practices which are subject to change. For these reasons, this material should not be relied upon as a substitute for specialized professional advice in connection with any particular matter.

Although this communication has been carefully prepared, Wilkinson & Company LLP does not accept any legal responsibility for its contents or for any consequences arising from its use. No part of this document may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means (photocopying, electronic, mechanical, recording or otherwise).