Real Estate Agents – Incorporating

Real estate agents would typically be operating as a “sole proprietor”, meaning all commission income earned would be reported on their personal tax returns, subject to their marginal tax brackets. Due to some legislative changes that occurred this year, a real estate agent now has the ability to incorporate their proprietorship on or after October 1, 2020. The resultant corporation is referred to as a Personal Real Estate Corporation (PREC).

What does it mean to incorporate?

“Incorporating” is the process of setting up a corporation. The corporation is a separate legal entity (i.e. “person”) from the realtor. This means that all income and expenses related to the real estate agent’s operations would be the corporation’s moving forward. As a shareholder / employee of the corporation, the real estate agent would need to decide how much compensation they are taking out of the corporation (dividend and/or salary) and how much money they are leaving in the corporation.

Every situation is different, and we strongly encourage an agent who is thinking of incorporating to reach out to their accountant and lawyer, in order to (1) ensure the corporation is set up properly; and (2) ensure all necessary elections and documentation are in place before operations begin in the corporation.

Why incorporate?

While there may be non-tax reasons to incorporate, we will focus on the primary tax benefits:

Tax deferral

Incorporating can provide a significant amount of tax deferral. A corporation pays a relatively low tax rate (12.2% or 26.5%) compared to the highest marginal personal tax rate of approximately 54%. This means that a corporation has more after-tax money to reinvest than an individual would otherwise have available.

When a corporation pays the real estate agent personally, the agent incurs personal taxes on the income received from the corporation. Ultimately when dealing at the highest marginal personal tax rates, a corporation that earns money and pays it out to a shareholder will pay approximately the same aggregate amount of tax (corporate + personal) that an individual would pay if they were earning that money without a corporation.

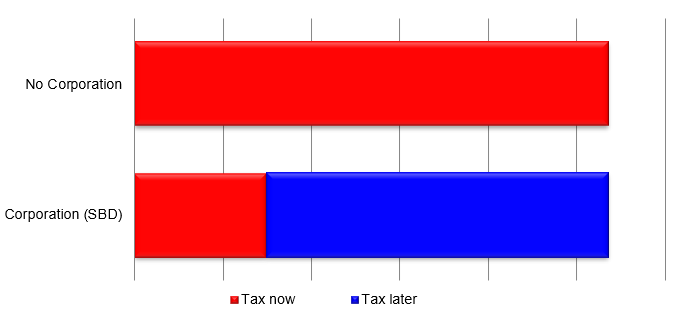

To illustrate, the following chart compares the amount of tax an individual would pay with no corporation, and the amount of tax that would be due by an individual with a corporation:

Note that the total amount of tax is comparable in both situations, however, the “blue” portion represents tax that is paid “later”, meaning that money can be reinvested and have a greater earning potential than the alternative of not having a corporation.

Tax savings – income smoothing

The above illustration of tax deferral assumes that someone is always in the highest tax bracket. In reality, this may not always be the case. A corporation allows for the individual to control how much income they receive in a particular year, and therefore have more control of what personal tax bracket they would fall within.

For example, say a real estate agent has a “good year” and a “bad year”. An agent without a corporation in the good year would potentially have income falling in the highest tax bracket, and would be paying more tax. In the bad year they would potentially have lower tax brackets going unused as income wasn’t sufficient to reach those.

A real estate agent with a corporation can average out their income over the years, to maximize the use of those lower tax brackets. The corporation would retain some of the profits from the good year and distribute them out in the bad year in order to minimize the high brackets used in the good year and maximize the lower tax brackets in the bad year.

Tax savings – splitting

Family members of the real estate agent can own certain non-voting shares of the corporation. This provides the corporation with the opportunity to compensate family members by way of dividend. Dividends paid to lower income family members provide the opportunity to use their lower personal tax brackets.

There are restrictions on how much of a dividend a corporation could pay a family member of the active shareholder. For the most part, compensation (dividend and/or salary) paid to a family member over age 24 has to line up with a reasonable amount for the work they perform for the corporation. Anything in excess would be taxed at the highest marginal tax rates. This result is referred to as Tax on Split Income (TOSI). For any family member 18-24, special rules apply to limit the amount of dividends to a “safe harbor” return on invested capital. As a result, compensation to family members under 25 usually needs to take the form of a reasonable salary or wage.

There are exceptions to the restrictions. If an adult family member is working on average more than 20 hours a week for the corporation in the particular year or any five previous years, there is no limitation on the amount of dividend that can be paid to them. Furthermore, if the dividend is paid to the spouse of the active shareholder and the active shareholder is over 65, there is no limitation on the dividend.

These exceptions provide some potential additional tax savings, particularly when it comes to retirement planning, for the incorporated real estate agent.

When not to incorporate?

Incorporating is not for everyone. There is a greater compliance burden with having a corporation as it requires separate reporting from the real estate agent, which comes with more paperwork and more costs.

In addition, if a real estate agent needs almost every dollar they earn to use personally, and no money is being saved, then they are not benefitting from tax deferral or tax savings, and ultimately are likely paying the same amount of tax that they would have paid without a corporation, plus additional compliance costs for having a corporation. Regardless, there may still be legal reasons to incorporate, and we would recommend discussing the matter with your lawyer.

Contact your accountant

Every person’s situation is unique, and the new legislation does have some restrictions on the ownership structure and the operations of the PREC. An accountant can help you with your personal tax planning to ensure that the benefit of the corporation outweighs the potential compliance costs and can assist with setting up a structure that aligns with your needs.

If you have any questions relating to this matter, contact your tax professionals at Wilkinson & Co. LLP

This publication is a general discussion of certain tax matters and should not be relied upon as professional advice. If you require tax advice, we would be pleased to discuss the issues in this publication with you, in the context of your particular circumstances.