CLIENT UPDATE – July 22, 2020 Significant Expansion of the Canada Emergency Wage Subsidy

We are contacting you today to inform you about the significant expansion and extension for the Canada Emergency Wage Subsidy (CEWS). After several weeks of speculation, the government announced the details of their proposed expansion of the CEWS on July 17, 2020.

The current incarnation of the program provides a wage subsidy of 75% of eligible wages for employers that have suffered a 30% decline in revenue. The original timeframe was March 15th to June 6th but was previously extended to August 29th.

There were several concerns with the existing program such as eligibility being an “all or nothing” test, the high cost of the program, and whether it was long enough to meet it s objectives.

Generally, the proposed changes will extend the program until November 21, reduce the subsidy rate gradually over that time and allow any employer that has had any decline in revenue to qualify. The subsidy rate will be reduced if the employer’s revenue decline is less than 50%. There is also a mechanism to provide a greater “top-up” subsidy to those employers with a revenue decline of more than 50%.

In addition, several measures are proposed that are discussed in more detail later in this document including:

- Changes for non-arm’s length employees and furloughed employees;

- Providing a mechanism to account for business amalgamations, incorporations and sales;

- Adding an appeal process when the employer disagrees with CRA’s rulings;

- Other technical amendments for non-profits, charities, and trusts

These are proposals that still need to be ratified by parliament and as such may not be implemented or may be different than the material in the announcement. If these changes are enacted, the expected cost of the CEWS is $83.6 billion.

The process of determining eligibility, calculating, and applying for the CEWS under the current program is already difficult. Our initial impression of these proposals is that it will become more difficult to undertake that process. We are here to help you and have a dedicated team that can assist you with the application process.

DETAILED ANALYSIS OF THE PROPOSALS

The Qualifying Periods and Reference Periods

Including the three original periods, the “qualifying periods” will be:

Period 1: March 5 – April 11

Period 2: April 12 to May 9

Period 3: May 10 to June 6

Period 4: June 7 to July 4

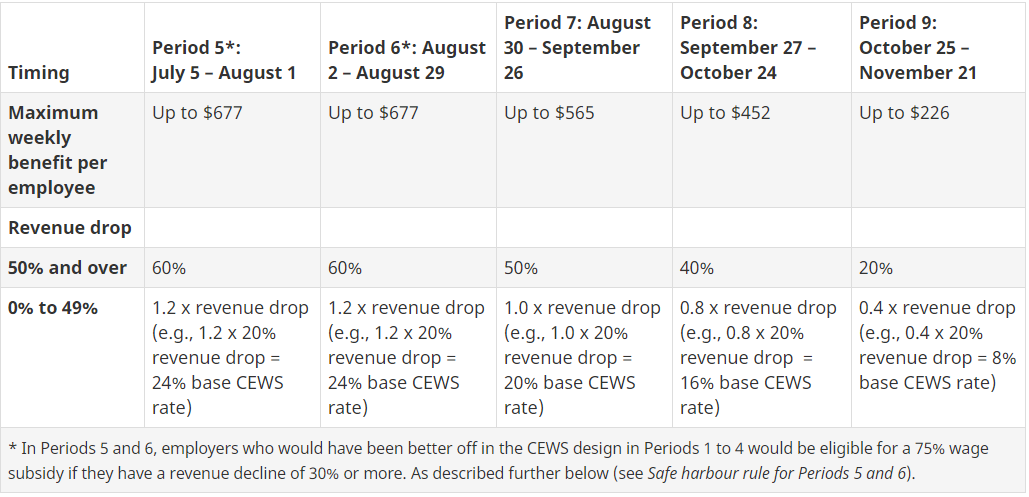

Period 5: July 5 – August 1

Period 6: August 2 – August 29

Period 7: August 30 – September 26

Period 8: September 27 – October 24

Period 9: October 25 – November 21

Another period from November 22nd to December 19th is also being considered.

The “reference period” is the period used to determine the percentage drop in revenue. In the existing program this was the same month in the previous year, or the average of January and February 2020. Under the proposed changes, employers for periods 6 to 9 would be able to compare one of two months for each period. For example, in period 7 an employer can compare their September 2020 revenues to September 2019 or, instead, choose to compare their August 2020 revenues to August 2019 to determine their eligibility.

This choice replaces the provision for periods 1 to 4 which automatically qualifies an employer for the period subsequent to one that did qualify for. For example, if an employer had a 40% drop in revenue for period 2, they automatically qualify for period 3 even if there was no revenue decline in period 3.

Under the existing provisions, once an employer chose between comparing monthly revenues to the prior year or comparing to the average of January and February 2020, they were required to continue with that election for all future months. The proposals now allow employers to change that election for period 5 and all subsequent periods. For instance, an employer who compared their revenue to the prior year in periods 1 to 4 could elect to compare to the average of January or February 2020 for all of periods 5 to 9.

The reference periods for periods 5 to 9 are summarized in the following chart:

The Base Subsidy

The 75% subsidy rate would be replaced with two new subsidy rates, a base subsidy of up to 60% and a top up subsidy of up to 25%.

The base rate will commence with a maximum subsidy rate of 60% in period 5 that will gradually decline to 20% by period 9. The maximum base subsidy is then further reduced if the employers decline in revenue is less than 50% of the prior refence period. The decline in the rate is determined by a formula that will decrease the subsidy rate for each percentage point drop in revenue that is less than 50%. This means that an employer with a 20% drop in revenue would still be eligible for the subsidy, but only at a rate of between 24% and 8%, depending on the month.

As a result of the lower subsidy rate, the maximum weekly benefit for each employee will drop from $847 as shown in the chart below.

However, a safe harbour rule applies for periods 5 and 6, an employer that would have received a higher subsidy under the existing 75% subsidy may claim that rate instead of the proposed one. This should be the case for most employers with a revenue decline of 30% or more.

Top Up Subsidy

An additional subsidy is available for employers that have experienced a drop in revenue of more than 50%. The maximum top up subsidy is 25% but will be less for employers with a revenue of drop of between 70% and 50%. Technically this is calculated at 1.25 times the revenue decrease in excess of 50%. A 60% drop in revenue would result in a top up subsidy of 12.5%. Unlike the base subsidy, this rate does not decrease in reference periods subsequent to period 6.

The refence period for the top-up subsidy is different than the reference period for the base subsidy. For the top-up subsidy, employers will compare either:

- The revenue in the previous 3 months in 2020 to the same three months in 2019; or

- The average monthly revenue for the previous 3 months to the average monthly revenue in January and February 2020.

When the top up rate is combined with the base subsidy, the maximum possible wage subsidy is 85% with a weekly maximum of $960 (60% base rate plus 25% top-up). This would be the case for an employer with a revenue decrease of 70% or more in periods 5 or 6

Eligible Employees

Under the existing rules employee are eligible for the subsidy if they are paid for the period and there was no period of 14 days that they were not paid for.

The proposals will eliminate the 14-day requirement for periods 5 to 9 such that any arm’s length employee should qualify if they are paid wages in respect of a period.

The current rules indicate that a non-arm’s length employee’s subsidy is also limited by their “baseline remuneration” which is their average weekly age from January 1, 2020 to March 15, 2020. This means that many such employees are not eligible as they are paid by way of dividends or annual bonuses. The proposals help with that issue but do not correct it entirely.

The new proposals allow employers to choose different periods in 2019 for the baseline remuneration. These changes may apply to both non-arm’s length and arm’s length employees. For arm’s length employees, this election may be beneficial if their wages in the 2019 periods are higher than they were in January to March 15, 2020.

- For period 4, they may elect to use the average weekly wage between March 1, 2019 and June 30, 2019 to calculate baseline remuneration;

- For subsequent periods they can elect to use the average weekly wage between July 1, 2019 and December 31, 2019 to calculate baseline remuneration;

Furloughed employees are currently eligible for CEWS and employers also receive a bonus subsidy for the employer portion of EI and CPP. The discussion in the news release indicates for periods 5 to 6 furloughed employees will continue to be eligible for a 75% subsidy rate (instead of 60%). For periods 7 to 9, the CEWS for furloughed employees will be adjusted to better align with the CERB program.

Determining Revenue

Several provisions were added that change how employers determine revenue in certain situations.

To accommodate employers that have acquired at least 90% of the assets of another business, they can file a joint election to include the acquired business’s prior revenues in their calculations. Without adding those prior revenue, the acquiring company may not qualify for the CEWS. This provision should also apply to an incorporation of a business.

The current provisions allow employers to elect to use the cash method to determine if they meet the revenue tests. The proposals will also allow employers that use the cash method to elect to use the accrual method of determining revenue.

Lastly, a corporation formed on an amalgamation may use the combined revenue of the predecessor corporations to determine eligibility.

Other Technical Changes

Other changes included in the proposals include the following:

- An appeals process was added to challenge the decisions of CRA;

- Rules were added to accommodate employers that use a payroll service provider (and are not registered for payroll);

- The filing deadline extended to January 31;

- Trusts’ eligibility will be restricted in certain cases for periods 4 to 9 in certain situations:

- Tax exempt trusts will now only be eligible if it is a registered charity or another eligible tax exempt entity; and

- Trusts that are public institutions will only be eligible if they are a prescribed organization;

If you have any questions concerning the above, do not hesitate to contact us.

This summary deals with proposed matters that are complex and may not apply to particular facts and circumstances. As well, the material and the references contained therein reflect laws and practices which are subject to change. For these reasons, this material should not be relied upon as a substitute for specialized professional advice in connection with any particular matter.

Although this communication has been carefully prepared, Wilkinson & Company LLP does not accept any legal responsibility for its contents or for any consequences arising from its use. No part of this document may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means (photocopying, electronic, mechanical, recording or otherwise).